Five years into a $500,000 mortgage at 5%, you check your statement. You’ve made about $174,000 in payments, and your balance has dropped by… $57,000. The other $117,000 went to interest. This is the moment most people decide the system is rigged, and I understand why. It looks like the bank loaded all its profit into the early years, before you could escape.

It’s not rigged. It’s one small piece of math doing exactly what it says, and once you see it, you can’t unsee it. No conspiracy required.

The only rule in the whole system

Here is the entire mechanism: each month, you pay interest only on what you still owe. That’s it. There’s no schedule of interest sitting in a vault, no front-loading decision made in a boardroom. Interest this month equals your remaining balance times the monthly rate, freshly calculated, every single month.

Think of it as renting money. The balance is how much money you are renting, and interest is the rent. In year one of that $500,000 mortgage you’re renting almost the full $500,000, and at 5% the rent on that much money is about $2,062 a month. Your payment is about $2,908, so after paying the rent, only $846 is left to actually reduce what you owe. Nobody took the difference from you. You simply rented a very large amount of money this month, and rent was due.

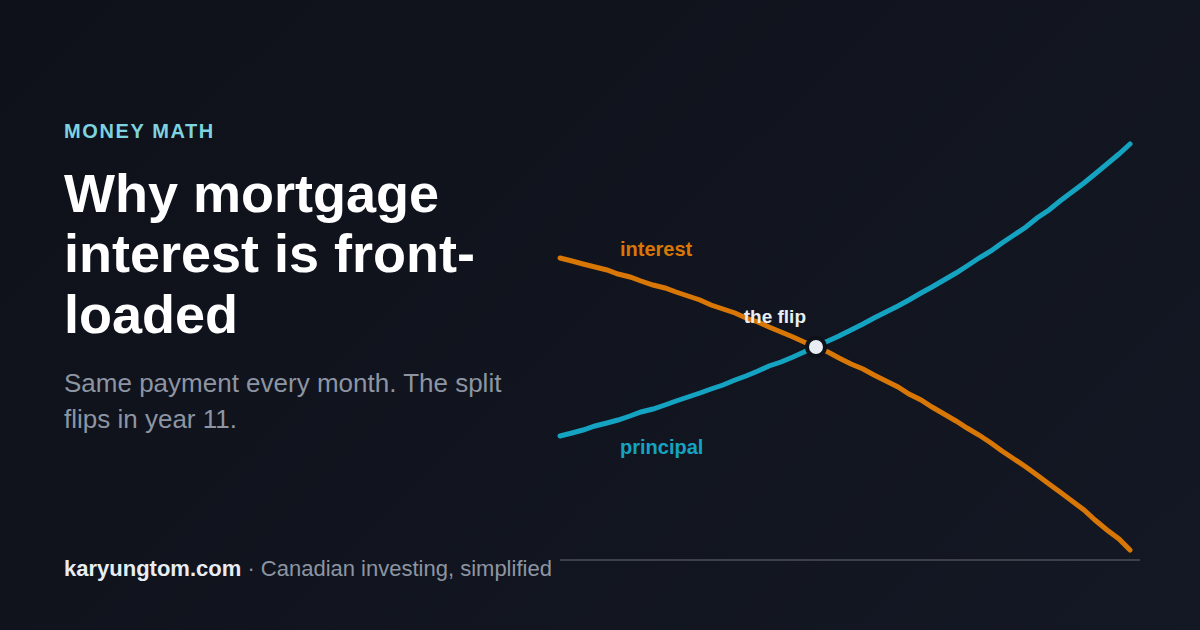

Now run the clock forward. Every payment chips the balance down a little, which means next month you’re renting slightly less money, which means the rent is slightly lower, which means slightly more of the same $2,908 goes to the balance. The process feeds itself. By the final years, you’re renting a small amount of money, the rent is tiny, and almost the whole payment lands on principal. The famous “front-loaded interest” curve is not a design choice. It’s just this one rule, repeated three hundred times.

The numbers, so you can check me

Take that $500,000 mortgage, 5%, amortized over 25 years. The payment is about $2,908 a month. Payment one splits into $2,062 interest and $846 principal. The split doesn’t reach 50/50 until year 11. Over the full 25 years you pay roughly $372,000 in interest on top of the $500,000 you borrowed. Those numbers feel outrageous in isolation, but each individual month is perfectly fair: you were charged 5% a year on exactly the amount you still owed, no more, no less.

Don’t take my word for it. Here is the whole thing, live. Change the numbers to your own mortgage and hover along the curve.

Show as a table

| Year | Balance | Interest / mo | Principal / mo |

|---|

The savings account mirror

If the front-loading still feels like a trick, flip it around. A savings account pays you interest on your balance. When the balance is big, you earn a lot; as you withdraw it down, you earn less each month. Nobody has ever accused a savings account of “front-loading” their interest earnings. It’s the identical mechanism with the direction reversed. A mortgage is just a savings account where you’re the bank’s customer on the wrong side of the counter.

“Fine, but why not split every payment evenly?”

Run the math on that. Splitting $500,000 evenly over 300 payments means $1,667 of principal a month, plus interest on whatever’s left. Month one: $1,667 plus $2,062 of interest, about $3,729 in total, and every payment after shrinks a little for 25 years. No Canadian lender sells that mortgage, and the first number is the reason: your biggest monthly bill would start at its maximum, exactly when most buyers are stretched thinnest. The level-payment mortgage smooths the same debt, the same rate, and the same renting-money rule into one predictable number. So the interest isn’t front-loaded to enrich the bank. The principal is back-loaded to protect your cash flow. Those are the same sentence read from two directions.

What this actually means for you

First, prepayments punch hardest early. An extra $10,000 in year two reduces the balance you rent for the next 23 years, so it kills far more total interest than the same $10,000 in year twenty. If the amortization curve bothers you, this is the lever: you can voluntarily turn your mortgage into something closer to the constant-principal version by prepaying early, and most Canadian lenders allow 10-20% a year without penalty.

Second, selling or refinancing after five years doesn’t mean you “wasted” your payments. You rented a large amount of money for five years and paid rent on exactly what you used. The math owes you nothing, and it took nothing.

Third, and this is the general lesson this site keeps circling: when a financial outcome makes you angry, work the arithmetic before assigning the blame. Sometimes there really is a villain. But most of the time it’s compound interest doing what it’s always done, indifferent to how it makes anyone feel. The math isn’t on anyone’s side, and that’s exactly what makes it worth learning.

Not financial advice, as always. If you’re weighing prepayments against investing, the comparison is your mortgage rate versus your expected after-tax return, and my cheatsheet covers how to think about that side of the ledger.